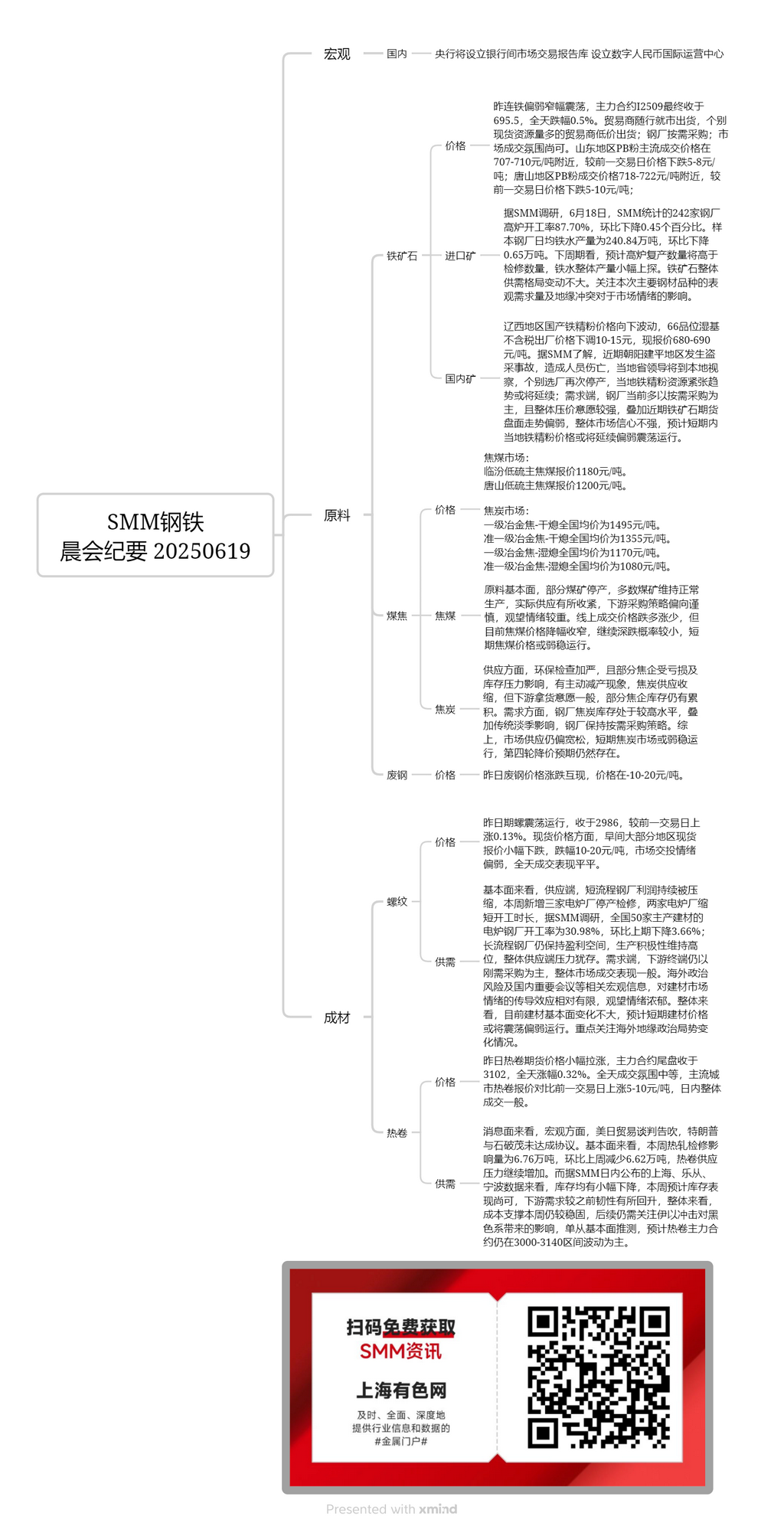

Domestic Ore:

In west Liaoning, the prices of domestically produced iron ore concentrates have declined, with the ex-factory price (66% grade, wet basis, excluding tax) falling by 10-15 yuan/mt, now quoted at 680-690 yuan/mt. According to SMM, a recent illegal mining accident occurred in Jianping, Chaoyang, resulting in casualties. Local provincial leaders are expected to visit the area, leading to the temporary suspension of operations at some beneficiation plants. This may exacerbate the tight supply of iron ore concentrates in the region. On the demand side, steel mills are primarily purchasing as needed, with a strong overall desire to bargain down prices. Coupled with the recent weak performance of iron ore futures, overall market sentiment remains weak. It is anticipated that iron ore concentrate prices in the region will continue to fluctuate rangebound in the short term.

Imported Ore:

Yesterday, DCE iron ore futures fluctuated rangebound in the doldrums, with the most-traded I2509 contract closing at 695.5, down 0.5% for the day. Traders sold according to market conditions, with some offering lower prices due to abundant spot resources. Steel mills purchased as needed, and the market trading atmosphere was moderate. In Shandong, the mainstream transaction prices of PB fines were around 707-710 yuan/mt, down 5-8 yuan/mt from the previous trading day. In Tangshan, PB fines were traded at around 718-722 yuan/mt, down 5-10 yuan/mt from the previous trading day. According to an SMM survey, on June 18, the operating rate of blast furnaces at 242 steel mills surveyed by SMM was 87.70%, down 0.45 percentage points MoM. The daily average pig iron production of the sampled steel mills was 2.4084 million mt, down 6,500 mt MoM. Looking ahead to next week, it is expected that the number of blast furnaces resuming production will exceed the number undergoing maintenance, leading to a slight increase in overall pig iron production. The overall supply-demand pattern of iron ore remains relatively unchanged. Attention should be paid to the impact of apparent demand for major steel products and geopolitical conflicts on market sentiment.

Coking Coal:

The quoted price of low-sulphur coking coal in Linfen is 1,180 yuan/mt. The quoted price of low-sulphur coking coal in Tangshan is 1,200 yuan/mt.

On the raw material fundamentals side, some coal mines have halted production, while most maintain normal operations, resulting in a slight tightening of actual supply. Downstream procurement strategies lean towards caution, with a strong wait-and-see sentiment. Online transaction prices have seen more declines than increases, but the current decline in coking coal prices has narrowed, and the probability of further significant declines is low. In the short term, coking coal prices may remain in the doldrums.

Coke:

The nationwide average price of premium metallurgical coke (dry quenching) is 1,495 yuan/mt. The nationwide average price of quasi-premium metallurgical coke (dry quenching) is 1,355 yuan/mt. The nationwide average price of premium metallurgical coke (wet quenching) is 1,170 yuan/mt. The nationwide average price of quasi-premium metallurgical coke (wet quenching) is 1,080 yuan/mt.

In terms of supply, environmental protection inspections have intensified, and some coking enterprises have voluntarily cut production due to losses and inventory pressure, leading to a contraction in coke supply. However, downstream purchase intentions are generally moderate, and some coking enterprises still have accumulated inventory. On the demand side, steel mills' coke inventory remains at a relatively high level. Coupled with the impact of the traditional off-season, steel mills maintain a purchasing-as-needed strategy. In summary, market supply remains relatively loose, and the coke market may remain in the doldrums in the short term, with the expectation of a fourth round of price cuts still existing.

Rebar:

Yesterday, rebar futures fluctuated and closed at 2,986, up 0.13% from the previous trading day. In terms of spot prices, most regions saw a slight decline in spot quotations in the morning, with a drop of 10-20 yuan/mt. Market trading sentiment was weak, and overall trading performance was mediocre throughout the day. On the supply side, the profits of EAF steel mills continue to be compressed. This week, three additional EAF plants have halted production for maintenance, and two have shortened their operating hours. According to an SMM survey, the operating rate of 50 EAF steel mills in China, which mainly produce construction materials, was 30.98%, down 3.66 percentage points from the previous period. Blast furnace steel mills still maintain profitability and high production enthusiasm, with ongoing pressure on the overall supply side. On the demand side, downstream terminals continue to make just-in-time procurement, with generally moderate overall market trading performance. The transmission effect of macro information such as overseas political risks and domestic important meetings on the sentiment of the construction materials market is relatively limited, with a strong wait-and-see sentiment. Overall, the fundamentals of construction materials remain relatively unchanged, and it is expected that construction materials prices may fluctuate in the doldrums in the short term. Close attention should be paid to changes in overseas geopolitical situations.

HRC:

Yesterday, HRC futures prices rose slightly, with the most-traded contract closing at 3,102, up 0.32% for the day. The trading atmosphere throughout the day was moderate, with mainstream city HRC quotations rising by 5-10 yuan/mt from the previous trading day, and overall trading performance being generally moderate. On the news front, macro-wise, US-Japan trade negotiations fell through, with Trump and Ishiba failing to reach an agreement. On the fundamentals side, this week, the impact from HRC maintenance was 67,600 mt, down 66,200 mt WoW, continuing to increase the supply pressure of HRC. According to data released by SMM during the day for Shanghai, Lecong, and Ningbo, inventories have all declined slightly. This week, inventory performance is expected to be moderate, and downstream demand has shown some resilience compared to before. Overall, cost support remains relatively stable this week. Subsequent attention should still be paid to the impact of the Israel-Iran conflict on the ferrous metals series. Based solely on fundamentals, it is expected that the most-traded HRC contract will continue to fluctuate mainly within the 3,000-3,140 range.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)